Part of the Hawksmoor Group

Part of the Hawksmoor Group

The Schroder Emerging Market Debt Total Return Fund was one of the lesser contributors in the quarter, but this belied its strong contribution during the first half of the year when emerging economies, having led in raising interest rates to combat inflation, were able to start cutting sooner than their developed market counterparts. The strategic and corporate bond funds all turned in good contributions.

Our small allocation to equities saw the new (September 2023) acquisition Guinness Global Equity Income Fund contributing positively, but RIT Capital struggled with the unprecedently high level of its discount to NAV. Some changes have occurred in its senior personnel recently and we shall be watching to what effect this has on investor confidence and performance. The fund remains an attractive source of private investment strategies (among more traditional investments) which we believe provides useful diversification.

The CPS’ Alternative category is as large as Cash & Bonds at 46% but much more diverse, and contributions towards the overall return were also all positive though with some significant variances. Our core infrastructure and gold investments benefitted from the better outlook for interest rates, while the multi-asset strategies maintained a steadier approach.

Looking out to 2024 and beyond, with the 2022-23 period of sharp adjustments hopefully largely behind us, it feels like we have still some way to go before equity valuations fully discount the return to ‘normal’ interest rate levels, despite the amazing performance of the Magnificent Seven in 2023. Bonds on the other hand seem to have largely made the correction and, barring a resurgence of the rampant inflation which came out of Covid and Ukraine, look more attractive than they have done for many years.

Alternatives are trickier to forecast, partly given the catch-all nature of the asset class’s description. Gold provides protection against inflation and geopolitical instability (of which there is no shortage). We expect the multi asset funds we hold all to provide to varying degrees something similar. To what extent the infrastructure funds can deliver attractive returns in a world of normalised interest rate policy and are not just a relic of the ‘alternative income’ theme during the era of ZIRP and QE, is something we shall be considering more closely when their discounts recover closer to NAV. While their real yields are undoubtedly attractive given the quality of the cash flows, their longevity is limited as long as discounts bar the raising of new capital.

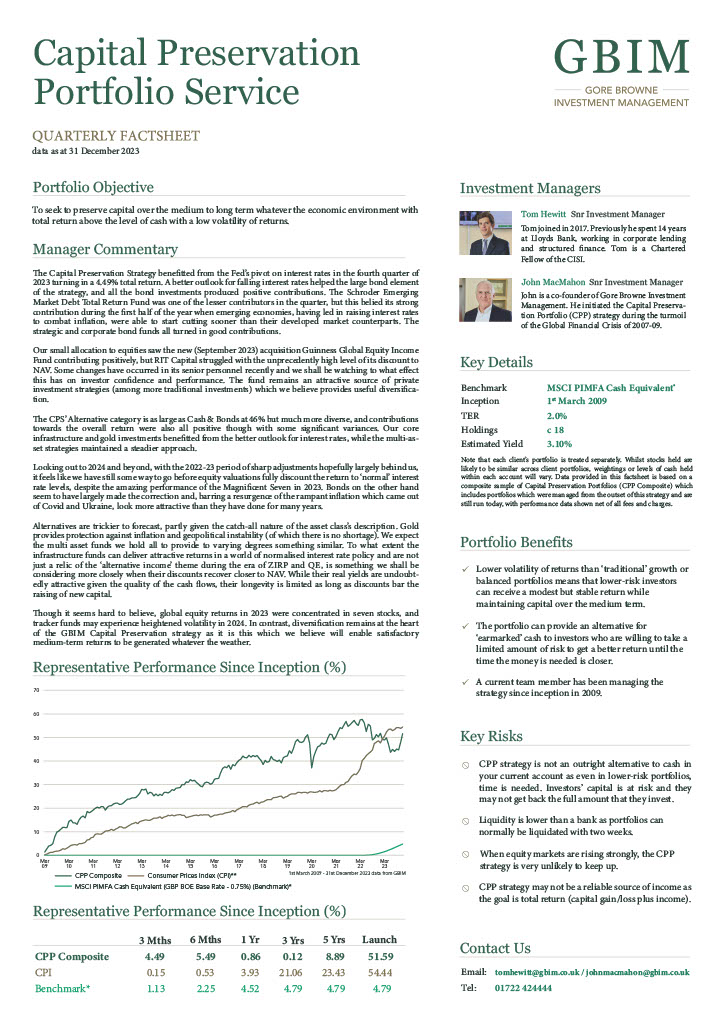

Though it seems hard to believe, global equity returns in 2023 were concentrated in seven stocks, and tracker funds may experience heightened volatility in 2024. In contrast, diversification remains at the heart of the GBIM Capital Preservation strategy as it is this which we believe will enable satisfactory medium-term returns to be generated whatever the weather.