Part of the Hawksmoor Group

Part of the Hawksmoor Group

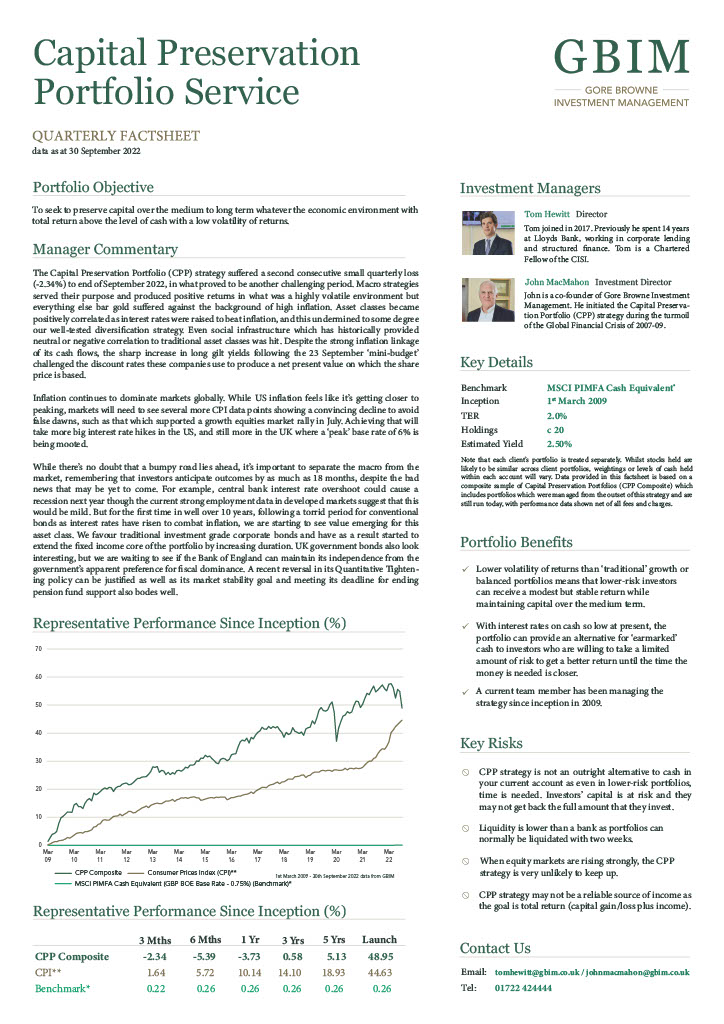

Macro strategies served their purpose and produced positive returns in what was a highly volatile environment but everything else bar gold suffered against the background of high inflation. Asset classes became positively correlated as interest rates were raised to beat inflation, and this undermined to some degree our well-tested diversification strategy. Even social infrastructure which has historically provided neutral or negative correlation to traditional asset classes was hit. Despite the strong inflation linkage of its cash flows, the sharp increase in long gilt yields following the 23 September ‘mini-budget’ challenged the discount rates these companies use to produce a net present value on which the share price is based.

Inflation continues to dominate markets globally. While US inflation feels like it’s getting closer to peaking, markets will need to see several more CPI data points showing a convincing decline to avoid false dawns, such as that which supported a growth equities market rally in July. Achieving that will take more big interest rate hikes in the US, and still more in the UK where a ‘peak’ base rate of 6% is being mooted.

While there’s no doubt that a bumpy road lies ahead, it’s important to separate the macro from the market, remembering that investors anticipate outcomes by as much as 18 months, despite the bad news that may be yet to come. For example, central bank interest rate overshoot could cause a recession next year though the current strong employment data in developed markets suggest that this would be mild. But for the first time in well over 10 years, following a torrid period for conventional bonds as interest rates have risen to combat inflation, we are starting to see value emerging for this asset class. We favour traditional investment grade corporate bonds and have as a result started to extend the fixed income core of the portfolio by increasing duration. UK government bonds also look interesting, but we are waiting to see if the Bank of England can maintain its independence from the government’s apparent preference for fiscal dominance. A recent reversal in its Quantitative Tightening policy can be justified as well as its market stability goal and meeting its deadline for ending pension fund support also bodes well.