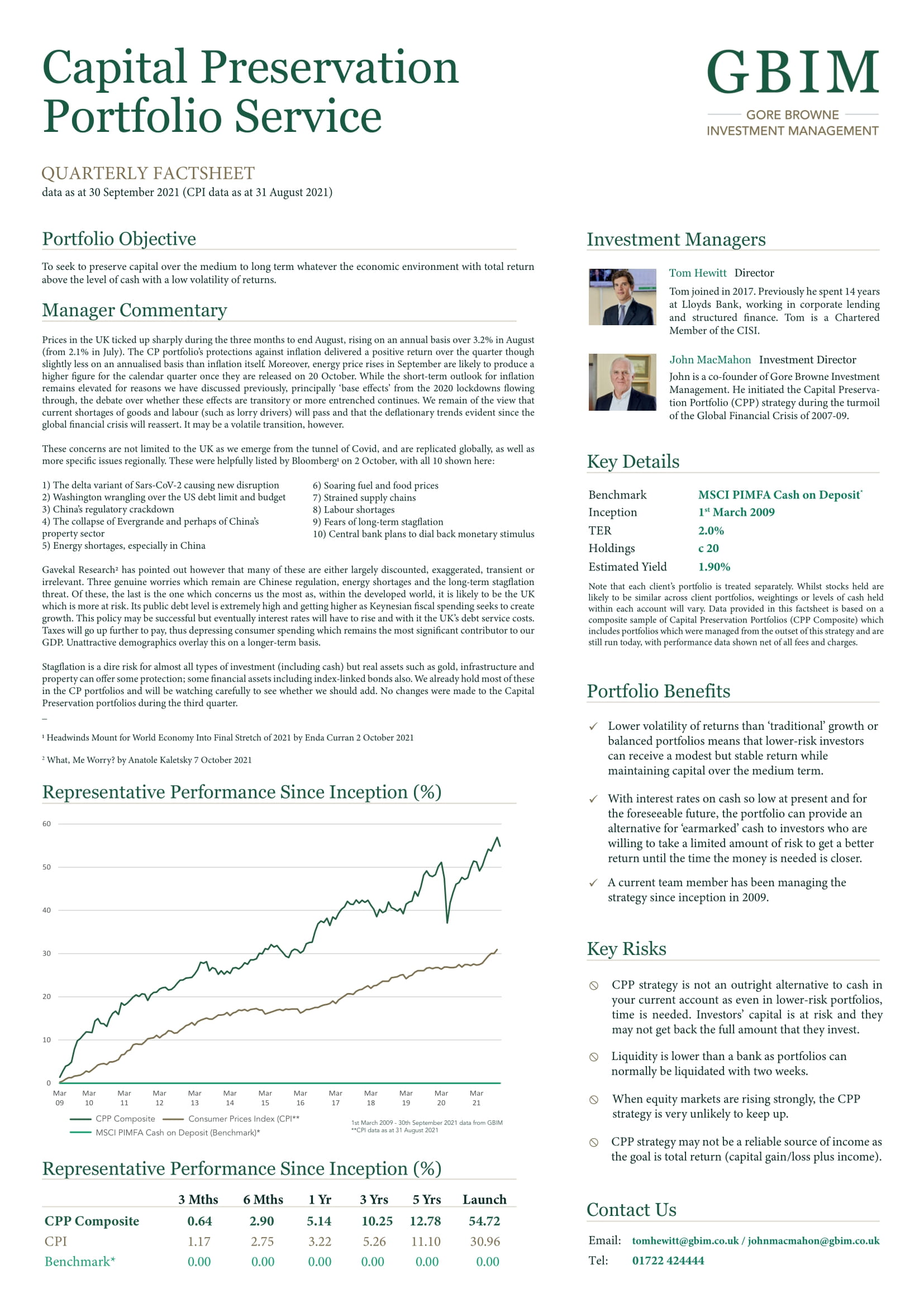

Part of the Hawksmoor Group

Part of the Hawksmoor Group

While the short-term outlook for inflation remains elevated for reasons we have discussed previously, principally ‘base effects’ from the 2020 lockdowns flowing through, the debate over whether these effects are transitory or more entrenched continues. We remain of the view that current shortages of goods and labour (such as lorry drivers) will pass and that the deflationary trends evident since the global financial crisis will reassert. It may be a volatile transition, however.

These concerns are not limited to the UK as we emerge from the tunnel of Covid, and are replicated globally, as well as more specific issues regionally. These were helpfully listed by Bloomberg1 on 2 October, with all 10 shown here:

1) The delta variant of Sars-CoV-2 causing new disruption

2) Washington wrangling over the US debt limit and budget

3) China’s regulatory crackdown

4) The collapse of Evergrande and perhaps of China’s property sector

5) Energy shortages, especially in China

6) Soaring fuel and food prices

7) Strained supply chains

8) Labour shortages

9) Fears of long-term stagflation

10) Central bank plans to dial back monetary stimulus

Gavekal Research2 has pointed out however that many of these are either largely discounted, exaggerated, transient or irrelevant. Three genuine worries which remain are Chinese regulation, energy shortages and the long-term stagflation threat. Of these, the last is the one which concerns us the most as, within the developed world, it is likely to be the UK which is more at risk. Its public debt level is extremely high and getting higher as Keynesian fiscal spending seeks to create growth. This policy may be successful but eventually interest rates will have to rise and with it the UK’s debt service costs. Taxes will go up further to pay, thus depressing consumer spending which remains the most significant contributor to our GDP. Unattractive demographics overlay this on a longer-term basis.

Stagflation is a dire risk for almost all types of investment (including cash) but real assets such as gold, infrastructure and property can offer some protection; some financial assets including index-linked bonds also. We already hold most of these in the CP portfolios and will be watching carefully to see whether we should add. No changes were made to the Capital Preservation portfolios during the third quarter.

_

1 Headwinds Mount for World Economy Into Final Stretch of 2021 by Enda Curran 2 October 2021

2 What, Me Worry? by Anatole Kaletsky 7 October 2021