Part of the Hawksmoor Group

Part of the Hawksmoor Group

This quarter was weak due to ongoing lockdowns in China which caused further disruptions to supply chains and affected companies such as Strix (kettle technology), Alliance Pharma (Kelo-Cote “scar product”), and Inspiration Health (ventilators for infants). However, supply chain pressures should be easing as China moves away from the zero-covid policy and re-opens its borders. Regrettably one of our companies, MJ Hudson (MJH), took the decision to ask for a temporary suspension of its shares due to delays in the submission of its audited FY22 accounts. We have since met with the CEO Mathew Hudson (who has a large shareholding in the business), and he confirmed that it was a revenue recognition issue rather than a cashflow issue. We expect a further update at the end of January/early February.

Cerillion, Zoo Digital, Lok’nStore, and Judges Scientific have been strong performers in our portfolio, and all produced results in line with or ahead of expectations. Zoo Digital, for example, is a provider of end-to-end cloud-based localisation and digital media services to the global entertainment industry. In 2021, $220bn was invested in content creation and we expect the content market to continue growing. For content creators (movies/tv series), language-related expenditure is a small portion of their overall cost base and insignificant relative to the potential returns of a more global audience for their content. Zoo Digital manages its capacity carefully and is not willing to commit if it can’t deliver. Furthermore, the company is protected from consumer recession and operates in a defensive B2B market.

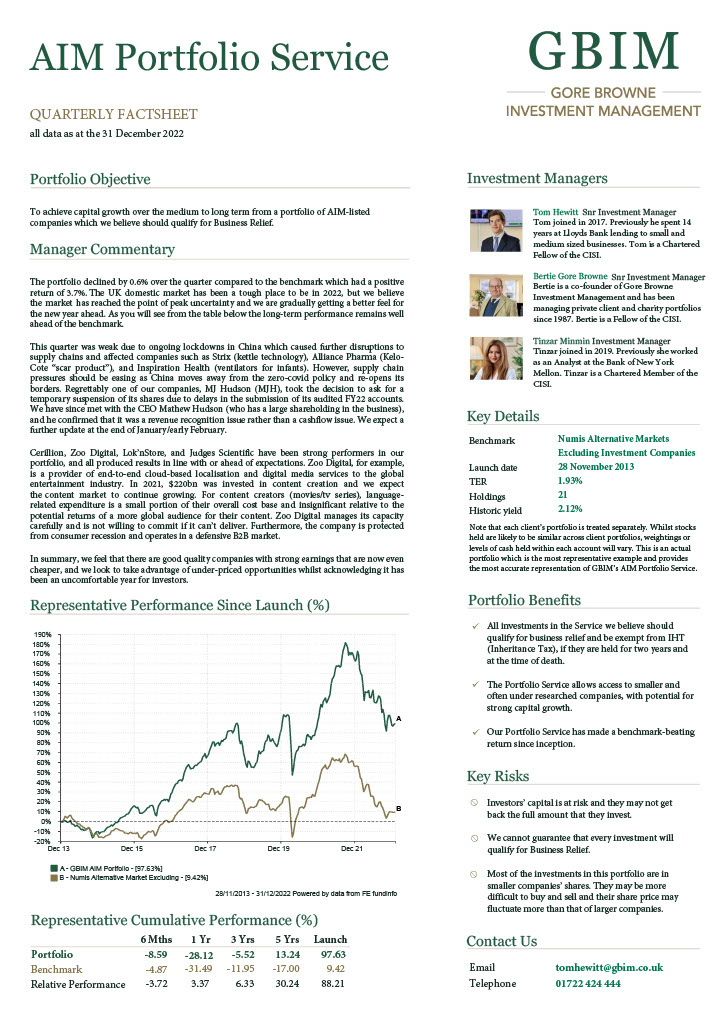

In summary, we feel that there are good quality companies with strong earnings that are now even cheaper, and we look to take advantage of under-priced opportunities whilst acknowledging it has been an uncomfortable year for investors.